In my last post I asked, "Is a promissory note considered a security?"

I further asked, "What does the SEC have to say?"

I then cited some information found on the SEC website that makes the statement:

"Most promissory notes must be registered as securities with the SEC and the states in which they’re being sold."

This morning I called SEC Toll-Free Investor Information Service at 1-800-SEC-0330. I easily reached a representative and explained the reason for my call. She made a statement along the lines of,

"Unless a Promissory Note is sold on an exchange it does not need to be registered with the SEC."

She then suggested I call the SEC Office of Small Business Policy. I'm not 100% on whether this is the most appropriate direction, but I took her advice and called.

The automated answer states, "If you have an interpretive or policy question" to leave a message and a lawyer will call back. So that's what I did. My question being:

"I have purchased Promissory Notes through the website, Prosper.com, a peer-to-peer lending site. Do these Promissory Notes require registration as securities with the SEC?"

(I explained that loans are "made" by WebBank, then "assigned" to Prosper, and then "assigned/sold" to individual investors)

I further asked:

"Is Prosper.com considered a broker/dealer of the Notes, and are they required to register as such with the SEC"

I will follow up on this.

Please sign the petition!

Ask a friend to sign!

Showing posts with label Prosper. Show all posts

Showing posts with label Prosper. Show all posts

Monday, September 22, 2008

Saturday, September 20, 2008

Is a Promissory Note considered a Security?

In my last post I left it with the question of:

Are the Promissory Notes that we are purchasing on Prosper considered Securities?

Well, nevermind Pennsylvania for now,

What does the SEC have to say?

Here's what they have to say about Promissory Notes:

Do The Notes Need To Be Registered?

Most promissory notes must be registered as securities with the SEC and the states in which they’re being sold. But remember that some promissory notes, such as those that have nine-month or shorter terms, may be “exempt.” That means that they don’t have to be registered. Since these notes fly under the radar screen of securities regulatory review, they have been the major source of investor complaints and fraudulent activity.

The above citation is available here (html) and here (pdf).

Are the Promissory Notes that we are purchasing on Prosper considered Securities?

Well, nevermind Pennsylvania for now,

What does the SEC have to say?

Here's what they have to say about Promissory Notes:

Do The Notes Need To Be Registered?

Most promissory notes must be registered as securities with the SEC and the states in which they’re being sold. But remember that some promissory notes, such as those that have nine-month or shorter terms, may be “exempt.” That means that they don’t have to be registered. Since these notes fly under the radar screen of securities regulatory review, they have been the major source of investor complaints and fraudulent activity.

The above citation is available here (html) and here (pdf).

What I noticed about these particular publications by the SEC is that they seem to be only talking about Promissory Notes issued by businesses as a means to raise capital.

I found another site here that discusses the problem with Promissory Notes:

They state that problems with promissory notes fall into three main categories:

Deception of Investors

The promissory note programs that are scams are often sold with the following deceptive statements: 1) investors would receive very high, double digit returns, 2) returns were guaranteed, and 3) the notes were backed by collateral to guarantee them. Frequently, a fraudulent promoter will persuade an independent life insurance agent, by offering very large commissions, to sell the notes to the agent's trusting customers. Often, promissory note schemes target the elderly and their retirement savings.

Unregistered Securities

Although those selling them may not know or admit it, these promissory notes are usually securities and must be registered with the SEC or the State they are sold in - or they must have a specific exemption from registration under the law. If the note is not registered, it will not be subject to review by regulators before it is sold, and investors have to do their own investigation to confirm that the company can pay its debt.

Unregistered Sellers

These promissory notes are usually securities, but those selling them often do not have the required securities sales license. If registered individual brokers are involved, they may be selling the notes without their firms' approval.

I definitely would not say that we are dealing with deception as described above. In general, Prosper lenders understand the risks, and Prosper goes to great length in the bidding process to point out the risk.

If anything, and as we're seeing in PA, it's boiling down to the registration of the notes, and maybe even the registration of Prosper, and maybe even the registration of WebBank, who is "assigning" the loans to Prosper who in turn "assigns" them to bidders.

Does "Assign" mean sell? It states in our Prosper Lender Agreement that we are "purchasing promissory notes". It says it plain and simple. It also says pretty clearly on the SEC website that "most promissory notes must be registered with the SEC and the state inwhich they're being sold."

For the first time all week, I'm beginning to feel a little better about Pennsylvania which is good, because I really do like PA.

I'll come back to this.

My kids are looking forward to going to Military Appreciation day at Kennywood this afternoon, and this stuffs been killing me all week, so honestly, I'm looking forward to it as well! But alas, I'm starting to feel like I'm understanding what's going on here.

Please sign the petition!

I Spoke with Pennsylvania Securities Commission

I spoke with Pennsylvania Securities Commission yesterday. As it turns out, they are in fact, the regulatory body Prosper is in discussions with.

I was really impressed and pleasantly surprised because they returned my call from Thursday. So my apologies to the Official Prosper Blog for doubting their statement of who they're in discussions with, and to the Commission for questioning their familiarity with the issue. I was hasty in my comments on Thursday, but in my defense, my blood pressure still hasn't returned to healthy levels yet.

Jill from the Commission was great, at least as great as she could be with obvious restraints on what she could say, and not personally having the power to make any problems go away.

She was knowledgeable of the issue. She was very easy to talk to, and she heard me out. That was refreshing, but like Prosper, because it's an open issue, she was not able to give me any specific details, or clue me in on what direction the issue is heading.

I was hoping to find out whether "Lending" on Prosper is something the Commission frowns upon, and wants to restrict it's citizens from doing, or is it just a matter of enforcing regulation, and Prosper taking steps to comply with state regulations. She couldn't answer the question of, "Are you guys for it, or against it?"

Her response was, "All I can say is that, any action the Commission takes is to protect the interest of Pennsylvania Investors."

Refer to page 6 of the Act if you would like to see where a "note" is defined as a Security.

It's safe to say, my conversation shed some new light on the situation.

In regards to the Pennsylvania Department of Banking, and the Loan Interest and Protection Law (Act 6 of 1974), and the Consumer Discount Company Act (Act 66 of 1937), I would say that these are NOT the regulations that are keeping me and yunz other Pennsylvania Lenders from doing our thing on Prosper. It is much more likely to be this.

Like Prosper said in their announcement, it has to do with Interpretation.

The Prosper Lender Agreement states that we are "making loan purchasing commitments" (bidding), and "purchasing promissory notes from Prosper". That is why in this post I say that it's a stretch on Pennsylvania's part in regards to the Department of Banking regulations.

The BIG question that comes to me is:

Are the Promissory Notes that we are purchasing on Prosper considered Securities?

Well yeah, according to Pennsylvania they are.

Am I satisfied with that?

NOPE -not yet.

By the way, where are all the Pennsylvania Prosper Lenders, and why haven't they signed the petition?

Please sign the petition!

Ask a friend to sign!

I was really impressed and pleasantly surprised because they returned my call from Thursday. So my apologies to the Official Prosper Blog for doubting their statement of who they're in discussions with, and to the Commission for questioning their familiarity with the issue. I was hasty in my comments on Thursday, but in my defense, my blood pressure still hasn't returned to healthy levels yet.

Jill from the Commission was great, at least as great as she could be with obvious restraints on what she could say, and not personally having the power to make any problems go away.

She was knowledgeable of the issue. She was very easy to talk to, and she heard me out. That was refreshing, but like Prosper, because it's an open issue, she was not able to give me any specific details, or clue me in on what direction the issue is heading.

I was hoping to find out whether "Lending" on Prosper is something the Commission frowns upon, and wants to restrict it's citizens from doing, or is it just a matter of enforcing regulation, and Prosper taking steps to comply with state regulations. She couldn't answer the question of, "Are you guys for it, or against it?"

Her response was, "All I can say is that, any action the Commission takes is to protect the interest of Pennsylvania Investors."

-Hey,

Thanks for the protection!

Glad to know you've got my back! As a personal standard, I love Government Intervention, especially when it protects me from earning good interest and using my money as I see fit for me. You're making me all warm and fuzzy.

Hey Government!!

How about protecting your citizens from ridiculous Credit Card Rates, Pay Day Loans, oh yeah, and how about the collection fee in excess of 24% of principle the Department of Education can charge, and then add to principle on student loan defaults.

Anyway, she really was helpful because she provided some information that was new to me. She did point out that there has been "no order issued against Prosper", but that Prosper is in violation of this specific regulation:

Pennsylvania Securities Act of 1972

Specifically, Section 1-201, Registration Requirement. This is on page 7 of the Act.

Refer to page 6 of the Act if you would like to see where a "note" is defined as a Security.

It's safe to say, my conversation shed some new light on the situation.

In regards to the Pennsylvania Department of Banking, and the Loan Interest and Protection Law (Act 6 of 1974), and the Consumer Discount Company Act (Act 66 of 1937), I would say that these are NOT the regulations that are keeping me and yunz other Pennsylvania Lenders from doing our thing on Prosper. It is much more likely to be this.

Like Prosper said in their announcement, it has to do with Interpretation.

The Prosper Lender Agreement states that we are "making loan purchasing commitments" (bidding), and "purchasing promissory notes from Prosper". That is why in this post I say that it's a stretch on Pennsylvania's part in regards to the Department of Banking regulations.

The BIG question that comes to me is:

Are the Promissory Notes that we are purchasing on Prosper considered Securities?

Well yeah, according to Pennsylvania they are.

Am I satisfied with that?

NOPE -not yet.

By the way, where are all the Pennsylvania Prosper Lenders, and why haven't they signed the petition?

Please sign the petition!

Ask a friend to sign!

Thursday, September 18, 2008

I Spoke with the PA Department of Banking

First off, I just want to mention that the Official Prosper Blog mentions that the "The regulatory body we’re primarily in discussions with is the Pennsylvania Securities Commission".

If that's the case, they, the PSC, are not aware of it! Because I called them first, and they sure had no clue in the world what I was talking about. And the sweetheart of a receptionist I spoke with worked her tail off to no avail, trying to locate someone who DOES have a clue. She finally resolved to send me a complaint form to fill out. I agreed to receive it for a reason I'll discuss further on.

She also told me that she was informed that it was more likely the PA Department of Banking that would be involved in the restriction. This coincided with Rep. Pallone's response in regards to the two regulations "cited as reasons for Prosper.com to discontinue accepting lender registrations" and accepting new bids from existing lenders.

So I gave the PA DOB a call.

They too had no clue what I was talking about. For some reason I was not surprised. So I did my best to explain the situation. At which point I was told that they discourage any type of involvement in Pay Day Loans. Pay Day Loans?

So I s-l-o-w-l-y and thoroughly explained the situation again, and provided a quick 101 on Prosper and P2P Lending. I also did my best to explain how the restriction impacts Lenders' investment:

If that's the case, they, the PSC, are not aware of it! Because I called them first, and they sure had no clue in the world what I was talking about. And the sweetheart of a receptionist I spoke with worked her tail off to no avail, trying to locate someone who DOES have a clue. She finally resolved to send me a complaint form to fill out. I agreed to receive it for a reason I'll discuss further on.

She also told me that she was informed that it was more likely the PA Department of Banking that would be involved in the restriction. This coincided with Rep. Pallone's response in regards to the two regulations "cited as reasons for Prosper.com to discontinue accepting lender registrations" and accepting new bids from existing lenders.

So I gave the PA DOB a call.

They too had no clue what I was talking about. For some reason I was not surprised. So I did my best to explain the situation. At which point I was told that they discourage any type of involvement in Pay Day Loans. Pay Day Loans?

So I s-l-o-w-l-y and thoroughly explained the situation again, and provided a quick 101 on Prosper and P2P Lending. I also did my best to explain how the restriction impacts Lenders' investment:

- We can't liquidate,

- We can't compound our earnings, and

- We can't grow our portfolio thus,

- We can't narrow the risk impact of any single loan (ie. is a single loan worth 10% of your portfolio, or is worth 1% of your portfolio?)

After a couple of transfers I was given to someone who requested that I send, in writing, an explanation of the situation, and that I would receive a follow up from there.

So, I am now in the process of composing a letter.

I plan on including some pertinent documentation, especially the Prosper Lender Agreement that clearly explains that "Lenders" on Prosper are not "making", or "providing" loans:

"Your role as a Prosper "Lender" is that of a loan purchaser, and your rights and obligations as a purchaser or prospective purchaser of loans originated in the Prosper marketplace are set forth below.

Although you are referred to in this Agreement and on the Prosper website as a "Lender," you are not actually lending your money directly to Prosper borrowers, but are, instead, making loan purchase commitments and purchasing promissory notes from Prosper, representing loans made by WebBank, a Utah-chartered Industrial Bank ("WebBank") to borrowers and subsequently assigned to Prosper. All loans originated through Prosper are made to borrowers by WebBank from its own funds, and then subsequently sold and assigned by WebBank to Prosper. Prosper, in turn, will sell and assign such loans to the winning bidder or bidders on the listing without recourse to Prosper. WebBank is the originating lender and all loans are made under its charter as a Utah Industrial Bank. Prosper uses the term "Lender" instead of "loan purchaser" for the sake of brevity and simplicity.

This Lender Registration Agreement is made and entered into between you and Prosper Marketplace, Inc. ("Prosper")."

I will be sure to post the letter I draft along with a list of any enclosures.

I would really like to include a copy of the petition, and I most likely will, but honestly, and despite the incredible value of every signature added so far, I think it's a little skimpy at this point to make much of an impact. So please, if you haven't signed yet please do so. If you have signed, then please email at least one of your pals asking them to sign.

I will be back with another post shortly on why I may file a complaint with the Securities Commission.

Please sign the petition!

Wednesday, September 17, 2008

How Many Pennsylvanians are Prosper Lenders?

A HUGE THANK YOU to Eric's Credit Community for posting the number of Pennsylvanians who are Prosper Lenders.

- Total Lenders From PA: 760 (296 of which have placed bids in the last 30 days)

- Total Money On Loan From PA Lenders: $1,026,354

Largest PA based Lenders:

- CapitalAssurance ($67,633)

- batblackburn ($62,897)

- rogierunr1 ($56,736)

Great information to know. Personally, I was hoping to see Oh, I don't know, like a million PA Residents lending on Prosper! But kidding aside, from what I can tell this equates to somewhere around .026% of the legal-aged population. Not a big chunk of the population.

So please, even if you are not a PA Lender, and especially if you're a PA Lender, we could really use your signature.

Response from Representative John Pallone

I received the following response from Representative John Pallone:

Quick Note: The links provided in Mr. Pallone's email do not work. I've posted functioning links at the bottom of this post.

----------------------------------------------------------

Sent: Wednesday, September 17, 2008 2:18:43 PM

Subject: PA Laws on prosper.com website

As per your request for the Pennsylvania laws or regulations that were cited as reasons for prosper.com to discontinue accepting lender registrations, I have the following information. According to the Pennsylvania Department of Banking, entities providing loans in Pennsylvania, such as those offered on prosper.com, are limited to charging an interest rate no higher than 6%. This maximum rate is mentioned in two separate Pennsylvania laws: The Loan Interest and Protection Law (Act 6 of 1974) http://ldp.legis.state.pa.us/WU01/LI/LI/US/1974/0/0006..HTM and The Consumer Discount Company Act (Act 66 of 1937) http://ldp.legis.state.pa.us/WU01/LI/LI/US/1937/0/0066..HTM.

I hope this information is helpful.

Legislative Office for Research Liaison

PA House of Representatives

House Box 202218

Harrisburg PA 17120-2218

----------------------------------------------------------

Well, first off, I just want to say thank you to Rep. Pallone for his quick response, and for directing us towards the governing legislation.

So he points out,

"According to the Pennsylvania Department of Banking, entities providing loans in Pennsylvania, such as those offered on prosper.com, are limited to charging an interest rate no higher than 6%."

Now I'm not an attorney, or anything like that, BUT the obvious seems to jump off the page, execute an inward flying somersault, land on my face, and squirm around a little bit. Here's what's obvious:

Prosper Lenders are not "PROVIDING" loans!

Loan's are "Assigned" to Prosper Lenders.

The loans are "provided" by WebBank, of Salt Lake City Utah.

Prosper Lenders, take a look at one of your Promissory Notes.

Section 15 states:

"Governing Law. This Note is governed by federal law and, to the extent that state law applies, the laws of the State of Utah."

Needless to say this is quite a stretch on the part of Pennsylvania.

Does this mean that no resident of Pennsylvania can purchase an existing note, of any kind, from anyone, or any bank that has an interest rate of greater than 6%? I don't know the answer to that, but I can't imagine that's the case.

What in the world is PA trying to do?! I really don't get it. I wonder if Pennsylvania wouldn't mind stepping in and blocking the 18% collection fee that the Department of Education allows their private collection agencies to collect on student loans that go into default. - I Doubt it!

I will be posting more responses as I receive them.

Updated:

The Loan Interest and Protection Law (Act 6 of 1974)

The Consumer Discount Company Act (Act 66 of 1937)

Please sign the petition!

Ask a friend to sign!

Quick Note: The links provided in Mr. Pallone's email do not work. I've posted functioning links at the bottom of this post.

----------------------------------------------------------

Sent: Wednesday, September 17, 2008 2:18:43 PM

Subject: PA Laws on prosper.com website

As per your request for the Pennsylvania laws or regulations that were cited as reasons for prosper.com to discontinue accepting lender registrations, I have the following information. According to the Pennsylvania Department of Banking, entities providing loans in Pennsylvania, such as those offered on prosper.com, are limited to charging an interest rate no higher than 6%. This maximum rate is mentioned in two separate Pennsylvania laws: The Loan Interest and Protection Law (Act 6 of 1974) http://ldp.legis.state.pa.us/WU01/LI/LI/US/1974/0/0006..HTM and The Consumer Discount Company Act (Act 66 of 1937) http://ldp.legis.state.pa.us/WU01/LI/LI/US/1937/0/0066..HTM.

I hope this information is helpful.

Legislative Office for Research Liaison

PA House of Representatives

House Box 202218

Harrisburg PA 17120-2218

----------------------------------------------------------

Well, first off, I just want to say thank you to Rep. Pallone for his quick response, and for directing us towards the governing legislation.

So he points out,

"According to the Pennsylvania Department of Banking, entities providing loans in Pennsylvania, such as those offered on prosper.com, are limited to charging an interest rate no higher than 6%."

Now I'm not an attorney, or anything like that, BUT the obvious seems to jump off the page, execute an inward flying somersault, land on my face, and squirm around a little bit. Here's what's obvious:

Prosper Lenders are not "PROVIDING" loans!

Loan's are "Assigned" to Prosper Lenders.

The loans are "provided" by WebBank, of Salt Lake City Utah.

Prosper Lenders, take a look at one of your Promissory Notes.

Section 15 states:

"Governing Law. This Note is governed by federal law and, to the extent that state law applies, the laws of the State of Utah."

Needless to say this is quite a stretch on the part of Pennsylvania.

Does this mean that no resident of Pennsylvania can purchase an existing note, of any kind, from anyone, or any bank that has an interest rate of greater than 6%? I don't know the answer to that, but I can't imagine that's the case.

What in the world is PA trying to do?! I really don't get it. I wonder if Pennsylvania wouldn't mind stepping in and blocking the 18% collection fee that the Department of Education allows their private collection agencies to collect on student loans that go into default. - I Doubt it!

I will be posting more responses as I receive them.

Updated:

The Loan Interest and Protection Law (Act 6 of 1974)

The Consumer Discount Company Act (Act 66 of 1937)

Please sign the petition!

Ask a friend to sign!

Spreading the word!

Pennsylvanians for Prosper Lending and the Petition are mentioned here.

Great post! I'm sure all Pennsylvania Lenders appreciate the attention you've given this. I know I do!

Wondering what people are saying? Take a look here.

I'm grateful for the signatures & excellent comments people have left on the petition.

Please sign the petition!

Ask a friend to sign!

Great post! I'm sure all Pennsylvania Lenders appreciate the attention you've given this. I know I do!

Wondering what people are saying? Take a look here.

I'm grateful for the signatures & excellent comments people have left on the petition.

Please sign the petition!

Ask a friend to sign!

Good Point.

This post is a revision I made to my first post:

Tom from Prosper Lending had a terrific comment to the fact that I have only been on Prosper for 3 months, and that my current returns are not a good reflection of the returns that most investors see over time. I absolutely agree with him. Three months is not a long time at all. I was just beginning to get my feet wet, and I realize I have been lucky so far.

"According to Eric's Credit Community, my Average Interest Rate is 33.27%. My Experian Estimated Return on Investment is 25.14%, and my EricsCC Estimated ROI is 33.03%."

I had been focusing my investments in riskier, higher return loans. My strategy was to build my portfolio like this to the point where any single loan was less than 2% of my overall portfolio, at which time I was going to begin scaling back on riskier loans for lower risk, lower return loans.

This is all the more reason I'm frustrated with the restriction. As of now I am not able to push my portfolio to the point I wanted. My loans are greater than 2% of my total portfolio. On average, they're more like 4.75%.

Plus, I lose the ability to compound my returns. It was more about where this was going than where I am.

Of all the risks I considered when deciding to lend on Prosper, the risk of PA regulation barring me from investing was honestly not one of them.

It's probably important to note that Prosper investing was a small fraction of my overall investing activities. I enjoyed hand picking my loans, and I was willing to assume such risk because I am intrigued by the concept of people investing in other people.

Please sign the petition!

Ask a friend to sign!

Tom from Prosper Lending had a terrific comment to the fact that I have only been on Prosper for 3 months, and that my current returns are not a good reflection of the returns that most investors see over time. I absolutely agree with him. Three months is not a long time at all. I was just beginning to get my feet wet, and I realize I have been lucky so far.

"According to Eric's Credit Community, my Average Interest Rate is 33.27%. My Experian Estimated Return on Investment is 25.14%, and my EricsCC Estimated ROI is 33.03%."

I had been focusing my investments in riskier, higher return loans. My strategy was to build my portfolio like this to the point where any single loan was less than 2% of my overall portfolio, at which time I was going to begin scaling back on riskier loans for lower risk, lower return loans.

This is all the more reason I'm frustrated with the restriction. As of now I am not able to push my portfolio to the point I wanted. My loans are greater than 2% of my total portfolio. On average, they're more like 4.75%.

Plus, I lose the ability to compound my returns. It was more about where this was going than where I am.

Of all the risks I considered when deciding to lend on Prosper, the risk of PA regulation barring me from investing was honestly not one of them.

It's probably important to note that Prosper investing was a small fraction of my overall investing activities. I enjoyed hand picking my loans, and I was willing to assume such risk because I am intrigued by the concept of people investing in other people.

Please sign the petition!

Ask a friend to sign!

What's being said, petitioner comments...

A huge Thank You to everyone who has signed the petition so far.

Each and every signature is important. I don't know what it will lead to, but I hope to see it continue to grow. I can definitely say that with each signature I feel less alone in my frustration.

I hope that borrowers & lenders alike will sign the petition. I also hope that Prosper members from other states will feel our pain in PA & sign as well.

Even if you did not, or do not participate on Prosper your signature is appreciated.

Prosper and other p2p lending sites provide a means for Americans to invest directly in other Americans.

Imagine if regulators suddenly deprived individual investors of the ability to invest in stocks, bonds, Forex, etc. and left these markets open only to institutional investors. For obvious reasons this would never occur, but it's nonetheless something to think about.

I thought I would share some of the comments people have made so far:

"This will not stand! Our freedom to invest in fellow Americans has been taken away from us! Only 2 states can not participate in prosper lending process. Give me my freedom back!"

"It is my right to lend money."

"This is ridiculous - I have yet to read the specific regulations at work here, or contact the relevant state legislators and regulators, but rest assured I will. This is a pure intrusion on the rights of the individual, not suprising in a state that keeps a stranglehold on many other innocuous things like, alcohol sales (Anybody wanna try to buy a bottle of wine after 5PM on Sunday?)"

"I want my freedom back to participate in lending through prosper.com immediately. What regulation, sponsored by what special interest, has caused the PA State Government to do this to prosper?"

"I am shocked that our own PA legislators would stop us from helping others through properly handled loans! This is a situation where EVERYONE is happy (lenders and borrowers alike). I would hate to think that I live in a state where that freedom and originality is purposely stopped. This is discrimination pure and simple. Shame on you, and by the way, I VOTE."

"This is very disappointing. I have a small LLC and this was to become a serious portion of the companies earnings. There was no warning. I am hoping this is but a temporary misunderstanding and lending can continue as before!"

"I urge the legislators to stop discriminating against peer to peer lenders in favor of the banking industry who charge outrageous rates."

Each and every signature is important. I don't know what it will lead to, but I hope to see it continue to grow. I can definitely say that with each signature I feel less alone in my frustration.

I hope that borrowers & lenders alike will sign the petition. I also hope that Prosper members from other states will feel our pain in PA & sign as well.

Even if you did not, or do not participate on Prosper your signature is appreciated.

Prosper and other p2p lending sites provide a means for Americans to invest directly in other Americans.

Imagine if regulators suddenly deprived individual investors of the ability to invest in stocks, bonds, Forex, etc. and left these markets open only to institutional investors. For obvious reasons this would never occur, but it's nonetheless something to think about.

I thought I would share some of the comments people have made so far:

"This will not stand! Our freedom to invest in fellow Americans has been taken away from us! Only 2 states can not participate in prosper lending process. Give me my freedom back!"

"It is my right to lend money."

"This is ridiculous - I have yet to read the specific regulations at work here, or contact the relevant state legislators and regulators, but rest assured I will. This is a pure intrusion on the rights of the individual, not suprising in a state that keeps a stranglehold on many other innocuous things like, alcohol sales (Anybody wanna try to buy a bottle of wine after 5PM on Sunday?)"

"I want my freedom back to participate in lending through prosper.com immediately. What regulation, sponsored by what special interest, has caused the PA State Government to do this to prosper?"

"I am shocked that our own PA legislators would stop us from helping others through properly handled loans! This is a situation where EVERYONE is happy (lenders and borrowers alike). I would hate to think that I live in a state where that freedom and originality is purposely stopped. This is discrimination pure and simple. Shame on you, and by the way, I VOTE."

"This is very disappointing. I have a small LLC and this was to become a serious portion of the companies earnings. There was no warning. I am hoping this is but a temporary misunderstanding and lending can continue as before!"

"I urge the legislators to stop discriminating against peer to peer lenders in favor of the banking industry who charge outrageous rates."

"I am a Pennsylvania resident who has retained Prosper Marketplace Inc. et al, to facilitate my ernest desire to provide monetary assistance to certain private individuals. I may, and have, freely proffered Uncollateralized Promissory Notes without an intermediary within and without the Commonwealth, why am I prohibited from retaining structured counsel of my choosing to suggest candidates to me, prepare the legal note for me, and act as servicing and accounting agent on my behalf, all as bot parties have agreed shall be pleasant and expedient?"

"I live in Pa and was very happy with lending through Prosper"

"This is outrageous. Without any notification or any means to liquidate an existing position. What incredible discrimination"

"What happened to the free enterprise system"

"This stinks to high Heaven"

"Typical Pennsylvania Land of Taxes nonsense. I feel SO fortunate that we have our wonderful legislators looking out for us! Hey, the bankers need somebody to give their payoff money to."

"Why is our state govt limiting opportunity."

"I have been using prosper since Nov. 2007 and enjoyed helping out fellow people who are in need of financial assistance. I scrapped together the funds I could and lent it out; however, this comes as a shock, dissapointment, and outrage. I have begun withdrawing my funds from Prosper as they are paid. I think this was a very unwise move on their mark."

"This outrage does need to be corrected. So, PA regulations regarding loans and rate caps are to protect the citizens? So how about going after those loan shark payday loans that average 400% APR or MORE!!!. Instead of doing the banking industries dirty business and putting a halt on a RELIABLE, NON-USURAY, FREE- MARKET such as PROSPER that BORROWERS and LENDERS alike are all in favor for why not let the economy prosper!!??"

"I feel that this is completely the wrong way to go. Free markets are supposed to do as they will, and having government step in, when not needed, is completely detrimental to this."

"this is bull&*&t"

"Remove the lending and borrowing restrictions facing peer-to-peer loan market in the state of PA. A free market system for loans in the state will only benefit investment and growth in a state that is attempting to re-develop itself as it faces the 21st century."

"I want to LEND"

"Totally disgusted with this situation."

"I have over 10K invested in Prosper, am receiving a decent return and helping people at the same time. It took a lot of time to get my portfolio to that point. I now will receive that 10K back in dribs and drabs over 3 years, making reinvesting more tedious, as most investments will require me to accumulate minimum initial payments. I was told by my state senator that it is to protect consumers. Well, the consumers are able to borrow via Webbank, so the "protection" aspect is a failure. But the investors are not being protected by this decision at all. Pennsylvania should do the right thing and allow us to invest our money as we see fit. At the very least, we should be allowed to reinvest our current principal and future earnings back into Prosper."

"Let the big financial institutions run wild unregulated and put the whole world economy in danger. But regulate the small grassroots lenders. Typical BS from politicians in the pocket of Big Finance."

"Yet another example of heavy-handed PA regulations."

"Please allow PA residents to loan money. Microlending and peer-to-peer lending is a positive force."

"It would increase my self esteem if I was able to help out other people instead of just asking for help from strangers."

"PA should be allowed to lend on prosper."

"I guess the banks are upset so this is how they controlled us, shut us down. Nice State."

"Thank You for setting this site up. I just learned of this matter this morning, very upsetting! What are some numbers I can call, or emails. Also can you direct me to some other safe peer to peer sites, incase this falls through. Again Thank You, Ken Larsen"

"I can understand limitation for usuary. Taking advantage of someone who needs money. But to completely limit any social lending is undemocratic."

"Please do not restrict my right to invest my hard earned, after tax money."

"This is interference with free enterprise and a blatant attempt by lobbying banks and legislators and regulators to hamper commerce and opportunity for individual citizens. The net effect of this is to hamper efforts by many Pennsylvanianst o find funding unavailable in commercial markets and to make it impossible for investors to get a fair return on their money. I will be working to help identify the legislators and officials responsible for this and engage in my own lobbying efforts to see that these individuals are voted out of office or are removed."

"Given the current economic environment and credit tightening, is it not prudent to give "main street" as many aveneues as possible to obtain credit. Plenty of PA citizens are willing to step up to the plate and help out those who are in need of credit."

"Talk about a SNAFU!!"

"What is the problem? It seems to be a bit capricius on our law makers part. Prosper lending is helping people borrow money that otherwise might not be available. Person to person lending is probably stepping on some bodies toes and they are telling their hatchet men(the politicians) to get us to stop. It seems to be a clear cut case of bigness vs the little guy."

"How can a state tell a person where he/she is allowed to invest their money?!"

"I have the right to lend money"

"I am a student in PA and rely on prosper as a means of income to pay off my student loans. I ended up having a little extra from last loan and I am investing to ease the pain. I am a good student and already have a job lined-up after graduation. I find it an outrage that pheaa has stop lending out money yet you shutdown the only means of free market low rate loans available. Pennsylvania you have really failed me a state and I am considering moving to NJ after graduation just because of this law. This needs to be changed immediately. Francisco Esqueda"

"I urge you to rethink this law. I am a small time investor wanting to help out people to stimulate the economy. This prevents people from getting the cash flow they need during this time of economic crisis."

"This is crazy. MBNA, Discover, Citibank and all their friends can charge upwards of 22% to lend money, but an individual resident of Pennsylvania cannot lend! Very anti-resident and pro big business. Legislatures better wake up..."

"I am outraged at this infringement!"

"Show me the Regulators!"

"It is appalling that in a time when so many people are in need of loans, PA regulators prohibit residents who have the money from lending to those who need it. They should be ashamed."

"I was shocked and disappointed at this restriction, which came completely by surprise. I am angry with both Prosper and the Pennsylvania government."

"Another case of the "Commonwealth" being about 100 years behind the times."

"PA once again finds itself standing in the way of commerce and capitalism. As a resident of Pennsylvania I am both ashamed and enraged that my state is so backwards in its economic policies. In this time of national economic crisis, leaders need to encourage any economic growth possible, not stifling opportunities for investment and available credit."

"Prosper works well for all parties. There is risk, we accept it. I personally would rather gamble on real people than on the horses or the slots or the "second most famous groundhog in PA"...the lottery. The lottery may "benefit older Pennsylvanians, Prosper benefits all."

"Robbed. Almost makes me want to move to Jersey ;)"

"Moneylenders are an important source of credit for a wide range of interests. These interests span from the father who lends his son a few dollars to start a lemonade stand to the financing of transnational corporations. Prosper is a venue that allows individuals to lend their money to others for a fee. Some of the borrowers are financially savvy business owners. Other borrowers are those who would normally be refused credit by most financial institutions because their income may be at or below the poverty threshold or whose credit score indicates that the borrower might be unable to repay the loan. In between these two extremes fall the vast majority. To all of these lenders should be allowed to lend their own money; and borrowers should be allowed access to credit at a fair interest rate commiserate with their credit risk."

Thanks to everyone who has supported Peer-to-Peer lending in Pennsylvania by signing the PA for Prosper Lending petition.

Please sign the petition!

Tuesday, September 16, 2008

Thanks for the info Prosper!

When I spoke with Prosper earlier today I was told that a thread had been started in the Prosper community and that a member of their legal team would be fielding questions.

The Prosper Blog offered this information:

"The regulatory body we’re primarily in discussions with is the Pennsylvania Securities Commission.

Contact information for the Commission and other key Pennsylvania government and regulatory officials is included in the following links:

Pennsylvania Securities Commission

http://www.psc.state.pa.us/investor/contact.html

Pennsylvania Governor Edward G. Rendell’s Office

http://www.portal.state.pa.us/portal/server.pt?open=512&objID=2998&mode=2

Pennsylvania Open for Business

http://www.paopen4business.state.pa.us/paofb/cwp/view.asp?a=3&q=440975

Pennsylvania House of Representatives

http://www.legis.state.pa.us/cfdocs/legis/home/member_information/email_list.cfm?body=H

Pennsylvania State Senate

http://www.legis.state.pa.us/cfdocs/legis/home/member_information/email_list.cfm?body=S "

That helps! Thank you Prosper.

Please sign the petition!

Ask a friend to sign!

The Prosper Blog offered this information:

"The regulatory body we’re primarily in discussions with is the Pennsylvania Securities Commission.

Contact information for the Commission and other key Pennsylvania government and regulatory officials is included in the following links:

Pennsylvania Securities Commission

http://www.psc.state.pa.us/investor/contact.html

Pennsylvania Governor Edward G. Rendell’s Office

http://www.portal.state.pa.us/portal/server.pt?open=512&objID=2998&mode=2

Pennsylvania Open for Business

http://www.paopen4business.state.pa.us/paofb/cwp/view.asp?a=3&q=440975

Pennsylvania House of Representatives

http://www.legis.state.pa.us/cfdocs/legis/home/member_information/email_list.cfm?body=H

Pennsylvania State Senate

http://www.legis.state.pa.us/cfdocs/legis/home/member_information/email_list.cfm?body=S "

That helps! Thank you Prosper.

Please sign the petition!

Ask a friend to sign!

Can't Lend on Prosper? Try this Instead.

Do you enjoy Lending on Prosper?

Do you live in Pennsylvania?

Well guess what?

You're Grounded! -from Lending on Prosper that is.

Here's something to do in the meantime:

Email these guys!

Pennsylvania State Senate

Officers of the Pennsylvania State Senate

Pennsylvania House of Representatives

Pennsylvania Governor Edward G. Rendell’s Office

Pennsylvania Open for Business

more to come . . .

Please sign the petition!

Ask a friend to sign!

Do you live in Pennsylvania?

Well guess what?

You're Grounded! -from Lending on Prosper that is.

Here's something to do in the meantime:

Email these guys!

Pennsylvania State Senate

Officers of the Pennsylvania State Senate

Pennsylvania House of Representatives

Pennsylvania Governor Edward G. Rendell’s Office

Pennsylvania Open for Business

more to come . . .

Please sign the petition!

Ask a friend to sign!

Response from Prosper Customer Support

I figured, first things first, so I emailed Prosper support to validate the notice I received.

Here's their response followed by original email:

I decided to remove the email because Prosper support basically regurgitated the notice I received, swiftly deflating my hopes that this was a spoof. Not a big deal though, it is what it is.

The problem does not lie with Prosper, it lies with whatever regulations, and special interest has caused the PA governement to force Prosper's hand as it has.

In addition to emailing prosper support, I also called. Part of me was still holding out hope that it was spoof! I spoke with Brian, who was really cool about the whole thing.

He explained that their legal department is working to lift this restriction. Although he couldn't offer any time frame, or point to any specific regulation.

Please sign the petition!

Ask a friend to sign!

Here's their response followed by original email:

I decided to remove the email because Prosper support basically regurgitated the notice I received, swiftly deflating my hopes that this was a spoof. Not a big deal though, it is what it is.

The problem does not lie with Prosper, it lies with whatever regulations, and special interest has caused the PA governement to force Prosper's hand as it has.

In addition to emailing prosper support, I also called. Part of me was still holding out hope that it was spoof! I spoke with Brian, who was really cool about the whole thing.

He explained that their legal department is working to lift this restriction. Although he couldn't offer any time frame, or point to any specific regulation.

Please sign the petition!

Ask a friend to sign!

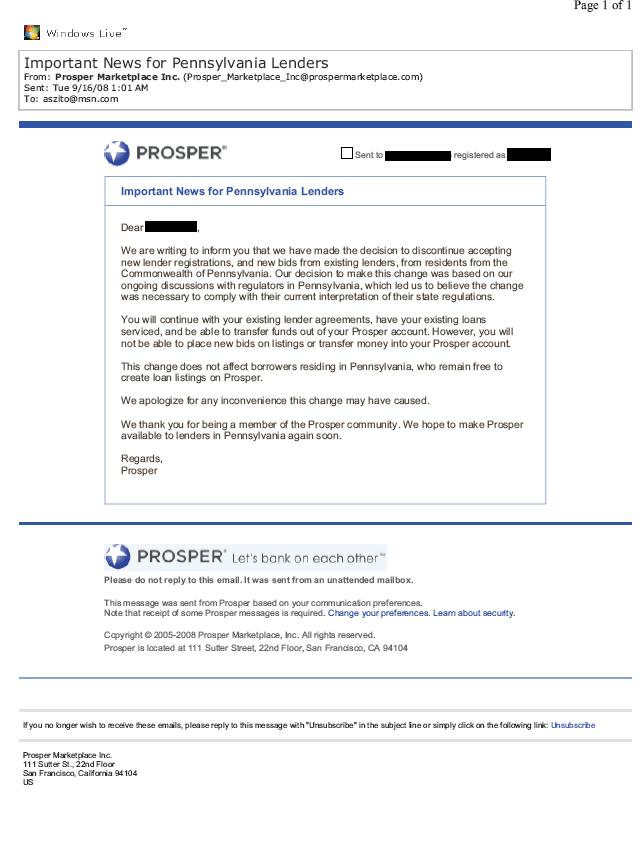

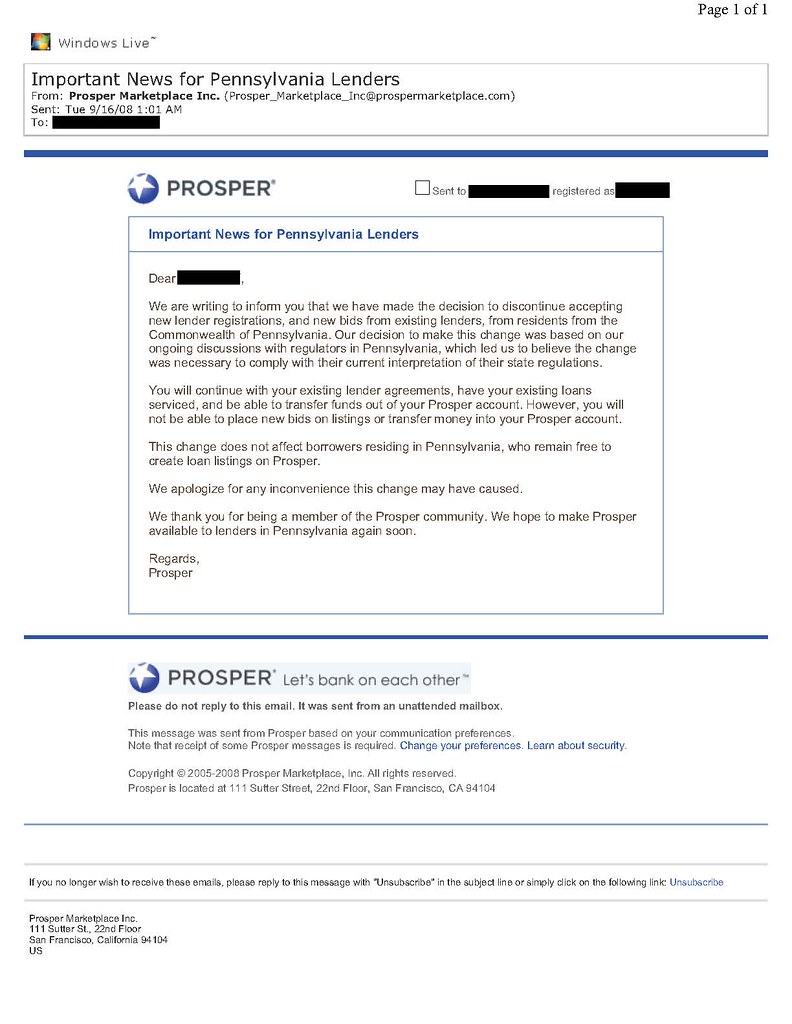

Important News for Pennsylvania (Prosper) Lenders

I am a Pennsylvania resident and I have been lending on Prosper for about three months. I love everything about being a Lender on Prosper.

Prosper creates a unique investment opportunity for individuals. It offers normal people a potential for excellent returns and the ability to help others.

I enjoy taking the time and hand picking the loans I bid on. Of my twenty-one Prosper loans, none of my borrowers have let me down yet. I also enjoy creating projections for my returns. Prosper is something that has become a new and favorite hobby of mine.

According to Eric's Credit Community, my Average Interest Rate is 33.27%. My Experian Estimated Return on Investment is 25.14%, and my EricsCC Estimated ROI is 33.03%.

Prosper creates a unique investment opportunity for individuals. It offers normal people a potential for excellent returns and the ability to help others.

I enjoy taking the time and hand picking the loans I bid on. Of my twenty-one Prosper loans, none of my borrowers have let me down yet. I also enjoy creating projections for my returns. Prosper is something that has become a new and favorite hobby of mine.

According to Eric's Credit Community, my Average Interest Rate is 33.27%. My Experian Estimated Return on Investment is 25.14%, and my EricsCC Estimated ROI is 33.03%.

(Revised: Tom from Prosper Lending had a terrific comment to the fact that I have only been on Prosper for 3 months, and that my current returns are not a good reflection of the returns that most investors see over time. I absolutely agree with him. Three months is not a long time at all. I was just beginning to get my feet wet, and I realize I have been lucky so far.

I had been focusing my investments in riskier, higher return loans. My strategy was to build my portfolio like this to the point where any single loan was less than 2% of my overall portfolio, at which time I was going to begin scaling back on riskier loans for lower risk, lower return loans.

This is all the more reason I'm frustrated with the restriction. As of now I am not able to push my portfolio to the point I wanted. My loans are greater than 2% of my total portfolio. On average, they're more like 4.75%.

Plus, I lose the ability to compound my returns. It was more about where this was going than where I am.

Of all the risks I considered when deciding to lend on Prosper, the risk of PA regulation barring me from investing was honestly not one of them.)

So, looking into the future, I am, or rather WAS, excited about the role Prosper Lending was going to play in my overall investment portfolio.

But, HERE'S THE PROBLEM:

This morning I woke up to find an email in my inbox from Prosper that knocked me off my chair, made me spill my coffee, spiked my blood pressure through the roof, and had me beating my steering wheel with open palm strikes the whole way to work.

The email basically told me that PA residents are no longer allowed to Lend on Prosper.

I feel robbed! -and needless to say, I'm furious. I'm not exactly sure how or where to direct my anger at this point.

So, for starters I created this blog on which to vent. I'm hoping other PA Lenders might stumble upon it. Please feel free to vent as well. Please! -share your thoughts, anger, or knowledge on this.

I will be doing everything I can to understand the Pennsylvania state regulations that are robbing me and other Pennsylvanians of this unique investment opportunity and I will be posting anything I learn here.

In the back of my mind I keep thinking that maybe this is some sort of spoof, and maybe it is. If so, it is the first Prosper Spoof I've ever received. I've emailed Prosper customer support to see if this is the case.

I really hope it is. If so, I owe my steering wheel an apology.

Subscribe to:

Comments (Atom)

{kind=link}

{kind=link}