Are the Promissory Notes that we are purchasing on Prosper considered Securities?

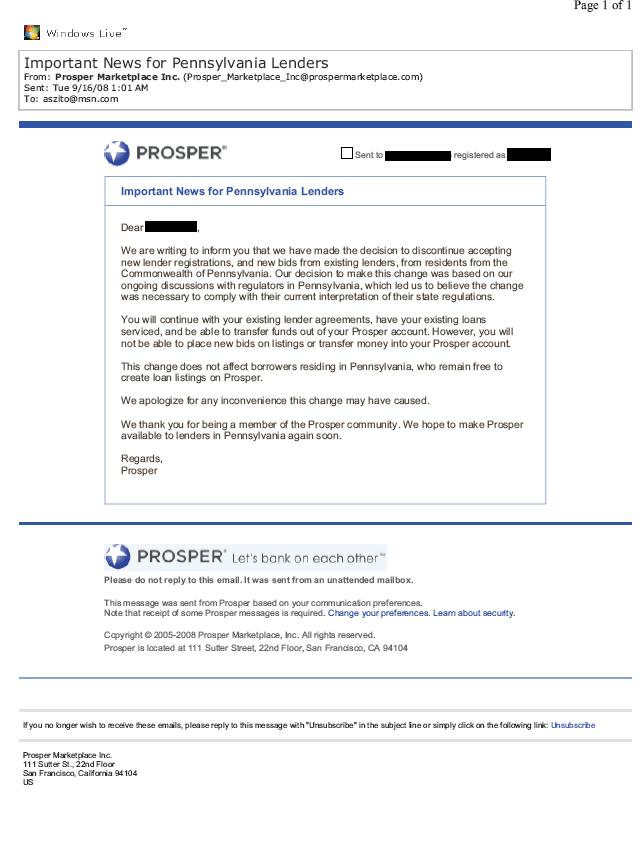

Well, nevermind Pennsylvania for now,

What does the SEC have to say?

Here's what they have to say about Promissory Notes:

Do The Notes Need To Be Registered?

Most promissory notes must be registered as securities with the SEC and the states in which they’re being sold. But remember that some promissory notes, such as those that have nine-month or shorter terms, may be “exempt.” That means that they don’t have to be registered. Since these notes fly under the radar screen of securities regulatory review, they have been the major source of investor complaints and fraudulent activity.

The above citation is available here (html) and here (pdf).

What I noticed about these particular publications by the SEC is that they seem to be only talking about Promissory Notes issued by businesses as a means to raise capital.

I found another site here that discusses the problem with Promissory Notes:

They state that problems with promissory notes fall into three main categories:

Deception of Investors

The promissory note programs that are scams are often sold with the following deceptive statements: 1) investors would receive very high, double digit returns, 2) returns were guaranteed, and 3) the notes were backed by collateral to guarantee them. Frequently, a fraudulent promoter will persuade an independent life insurance agent, by offering very large commissions, to sell the notes to the agent's trusting customers. Often, promissory note schemes target the elderly and their retirement savings.

Unregistered Securities

Although those selling them may not know or admit it, these promissory notes are usually securities and must be registered with the SEC or the State they are sold in - or they must have a specific exemption from registration under the law. If the note is not registered, it will not be subject to review by regulators before it is sold, and investors have to do their own investigation to confirm that the company can pay its debt.

Unregistered Sellers

These promissory notes are usually securities, but those selling them often do not have the required securities sales license. If registered individual brokers are involved, they may be selling the notes without their firms' approval.

I definitely would not say that we are dealing with deception as described above. In general, Prosper lenders understand the risks, and Prosper goes to great length in the bidding process to point out the risk.

If anything, and as we're seeing in PA, it's boiling down to the registration of the notes, and maybe even the registration of Prosper, and maybe even the registration of WebBank, who is "assigning" the loans to Prosper who in turn "assigns" them to bidders.

Does "Assign" mean sell? It states in our Prosper Lender Agreement that we are "purchasing promissory notes". It says it plain and simple. It also says pretty clearly on the SEC website that "most promissory notes must be registered with the SEC and the state inwhich they're being sold."

For the first time all week, I'm beginning to feel a little better about Pennsylvania which is good, because I really do like PA.

I'll come back to this.

My kids are looking forward to going to Military Appreciation day at Kennywood this afternoon, and this stuffs been killing me all week, so honestly, I'm looking forward to it as well! But alas, I'm starting to feel like I'm understanding what's going on here.

Please sign the petition!

{kind=link}